NPS vs UPS for Re-employed Ex-Servicemen : A Detailed Analysis

NPS vs UPS for Re-employed Ex-Servicemen: The introduction of the Unified Pension Scheme (UPS) has created significant interest among Central Government employees covered under the National Pension System (NPS). For re-employed ex-servicemen working in government departments, PSUs, autonomous bodies, and other civil organizations, the decision between NPS and UPS can have a major impact on retirement benefits.

Unlike regular civilian employees who may serve for 30 to 35 years, most ex-servicemen typically join civil employment after completing military service and can generally accumulate around 15 to 22 years of civilian service before retirement.

This raises an important question:

Should a re-employed ex-serviceman opt for UPS or continue under NPS?

Let’s examine the financial implications.

Understanding NPS and UPS

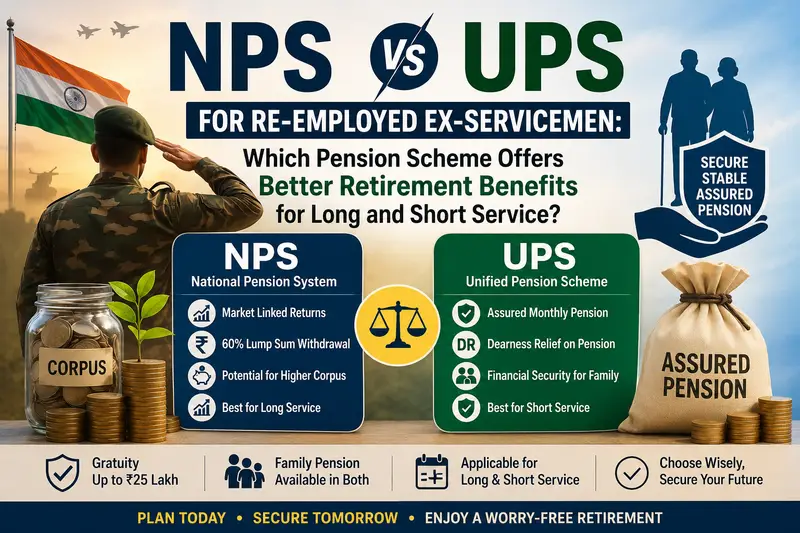

National Pension System (NPS)

NPS is a market-linked contributory pension scheme where:

- Employee and employer contribute every month.

- Retirement corpus depends on investment returns.

- 60% of the accumulated corpus can be withdrawn as a lump sum.

- 40% must be used to purchase an annuity for monthly pension.

- Pension amount is not guaranteed.

Unified Pension Scheme (UPS)

UPS provides:

- Assured pension based on qualifying service.

- Pension equal to 50% of average basic pay (subject to eligibility conditions).

- Dearness Relief (DR) on pension.

- Family pension benefits.

- Lump sum retirement benefit.

- Protection from market fluctuations.

Why Service Length Matters

The biggest advantage of NPS comes from long-term compounding.

Employees serving 30 to 35 years can build a very large retirement corpus through sustained contributions and market growth.

However, re-employed ex-servicemen generally have:

- Shorter civilian careers

- Lower contribution period

- Less time for compounding

As a result, NPS may not generate the same level of retirement corpus as it does for employees with 30+ years of service.

Estimated Comparison for 20 Years of Service

While exact figures depend on pay level, promotions, DA, and investment returns, the overall trend is clear.

| Parameter | NPS | UPS |

| Retirement Corpus | Depends on market performance | Not applicable |

| Monthly Pension | Based on annuity purchased from 40% corpus | Assured pension |

| Pension Stability | Market-linked | Guaranteed |

| Inflation Protection | Limited | Dearness Relief available |

| Lump Sum Amount | Generally higher | Relatively lower |

| Family Pension | Available | Available |

| Financial Risk | Higher | Lower |

Why UPS Appears More Beneficial for Most Re-employed Ex-Servicemen

1. Guaranteed Monthly Pension

UPS offers a predictable pension stream.

For ex-servicemen already receiving military service pension, a second assured pension from civil employment can create a strong and stable post-retirement income.

This becomes particularly valuable during economic uncertainty and fluctuating interest rates.

2. Shorter Service Period Favors UPS

Studies comparing NPS and UPS indicate that UPS becomes increasingly attractive when service duration falls below 25 years.

With only 20 years of civilian service, NPS contributions get less time to grow through compounding.

UPS, however, remains linked to salary rather than market performance.

3. Better Inflation Protection

UPS pension receives Dearness Relief (DR), helping retirees maintain purchasing power as inflation rises.

Under NPS, pension depends on annuity products that may not always provide comparable inflation protection.

4. Reduced Market Risk

NPS returns depend on:

- Equity market performance

- Debt market returns

- Fund management performance

UPS eliminates most of these uncertainties by offering a defined pension structure.

Where NPS Has an Advantage

Despite the benefits of UPS, NPS still offers some significant strengths.

Larger Lump Sum at Retirement

One of the biggest attractions of NPS is the ability to withdraw 60% of the accumulated corpus at retirement.

This lump sum can be used for:

- Purchasing a house

- Children’s education or marriage

- Medical emergencies

- Investment in fixed deposits or mutual funds

For financially disciplined retirees, this large corpus can generate additional income.

Greater Financial Flexibility

NPS provides more control over retirement funds and investment choices.

Employees who are comfortable with market-linked investments may find this flexibility appealing.

Pension Scheme (UPS) appears to offer a stronger overall retirement package due to its guaranteed pension, inflation protection through Dearness Relief, and reduced market risk.

While the National Pension System (NPS) can provide a larger lump-sum corpus, its advantages are generally more pronounced for employees with longer careers of 30 years or more.

Therefore, for veterans with shorter civilian service periods, UPS is likely to deliver better long-term financial security and a more stable post-retirement income stream.

However, the final decision should be based on individual factors such as expected service length, final basic pay, investment preferences, risk appetite, and existing military pension benefits.

Frequently Asked Questions (FAQs)

Is UPS better than NPS for ex-servicemen?

For most re-employed ex-servicemen with around 20 years of civilian service, UPS is generally considered more beneficial due to its assured pension and lower risk.

Can a re-employed ex-serviceman receive both military pension and UPS pension?

Yes. Military pension and civilian pension benefits are separate and can be received subject to applicable government rules.

Does UPS provide family pension?

Yes. UPS includes family pension provisions similar to other government pension systems.

Which scheme provides a larger lump sum amount?

NPS generally provides a significantly larger lump-sum payout because 60% of the accumulated corpus can be withdrawn at retirement.

Is gratuity different under UPS and NPS?

No. Gratuity benefits remain broadly similar under both schemes and are governed by applicable gratuity rules.