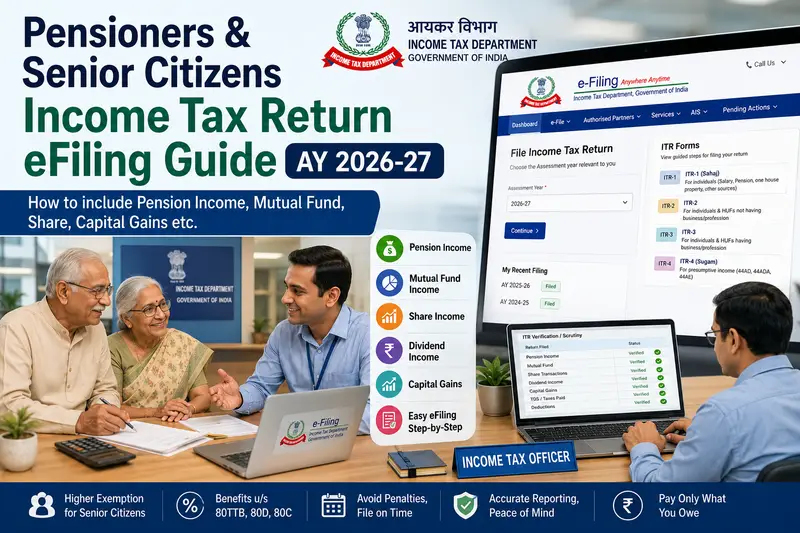

ITR: Zero tax preparation is not a given when one retires. Many pensioners continue to make money through investments, fixed deposits, savings accounts, and pensions. Senior citizens should review these perks and deductions to lower their taxable income before filing their ITR 2026.

Pension income is taxable

Many retirees rely on a combination of income from investments, bank interest, and pensions. Even though pension income is taxable, seniors can lower their taxable income by taking advantage of a number of deductions under the Income Tax Act.

Most deductions available to pensioners can be claimed only under the old tax regime. Under the new tax regime, taxpayers are generally not eligible for deductions under Sections 80C, 80D, 80DDB and 80TTB. However, the standard deduction continues to be available.

For resident individuals under the new tax regime, a rebate under Section 87A may also be available if taxable income falls within the prescribed limit.

Key deductions pensioners should know

Pensioners can claim a standard deduction from their pension income:

₹50,000 under the old tax regime

₹75,000 under the new tax regime

Since pension is taxed under the head “Income from Salary”, pensioners are eligible for this deduction.

Senior citizens can claim a deduction of up to ₹50,000 on interest earned from:

- Savings accounts

- Fixed deposits

- Post office deposits

Medical expenses often become a major retirement cost. Senior citizens can claim deduction for eligible health insurance premiums:

- Up to ₹50,000 for senior citizens

- Additional benefit may be available for health insurance premiums paid for senior citizen parents

Senior citizens can claim a deduction for treatment expenses related to specified diseases.

Senior citizens can claim a deduction of up to ₹50,000 on interest earned from:

- Savings accounts

- Fixed deposits

- Post office deposits

Medical expenses often become a major retirement cost. Senior citizens can claim deduction for eligible health insurance premiums:

- Up to ₹50,000 for senior citizens

- Additional benefit may be available for health insurance premiums paid for senior citizen parents

Senior citizens can claim a deduction for treatment expenses related to specified diseases.

- Up to ₹1 lakh for senior citizens (subject to applicable conditions)

Eligible deductions up to ₹1.5 lakh may include:

- Life insurance premium

- Provident Fund contributions

- NSC

- Housing loan principal repayment

6. Section 24(b): Home loan interest benefit

For taxpayers opting for the old tax regime:

Interest deduction up to ₹2 lakh may be available for a self-occupied house property, subject to conditions.

Other benefits pensioners should not miss

Individuals aged 80 years or above can continue filing ITR-1 and ITR-4 through paper mode, although online filing is also available.

For senior citizens, banks have a higher threshold before deducting TDS on interest income.

Pensioners should review their income sources, available deductions and tax regime choice before filing ITR 2026. Keeping documents such as Form 16, Form 26AS, AIS and investment proofs ready can make the filing process smoother.